Ⅰ. Introduction

In June 2025, the Japanese parliament enacted new legislation to establish a pre-insolvency workout framework. The official English title has not yet been determined, but it may be translated as the “Act on Financial Debt Adjustment Procedures for Enterprises to Facilitate Business Recovery” and is more commonly referred to as the “Early Business Recovery Act” (Act No. 67 of 2025, the “Act”). The Act will come into force by the end of 2026. In the meantime, relevant cabinet orders, ordinances by the Ministry of Economy, Trade and Industry (METI), and rules of the Supreme Court will be developed in preparation for the Act’s implementation.

Under this framework, a resolution concerning financial debt restructuring, such as debt reduction or rescheduling, will become legally binding, in principle, if it is passed by a supermajority vote of financial creditors—specifically, creditors representing at least 75% of the total voting rights at a creditors’ meeting—and is subsequently approved by the court. The framework adopts a hybrid structure that combines oversight by a neutral third-party organization with court approval, ensuring both expertise and procedural legitimacy. This dual-layered approach allows for an independent assessment of eligibility, feasibility, and creditor interests, followed by court validation of any supermajority-approved resolutions. Notably, the procedure is conducted, in principle, on a non-public basis, limiting potential reputational harm and operational disruption. This article outlines the economic background, procedural features and expected significance of the new regime1.

Ⅱ. Background of the Act

1. Economic Circumstances in Japan

Corporate debt in Japan has increased by about 120 trillion yen since before the COVID-19 pandemic. With ongoing challenges such as rising costs for raw materials and labor shortages, the number of bankruptcies in 2024 has surpassed 10,000 for the first time in 11 years. Given the continued depreciation of the Japanese yen, inflation, and labor shortages, there is growing concern that the debt burden will become a hindrance to business activities to improve profitability, causing companies to miss opportunities for business growth and leading to more bankruptcies.

In order to respond to these economic and social circumstances, it has been essential to establish a legal framework that enables enterprises at risk of financial distress to pursue early business recovery. Such a framework would enhance the economy’s ability to renew itself by facilitating smoother transitions and recoveries.

2. Challenges in the Current Debt Restructuring Tools in Japan

Japan’s current corporate debt restructuring regime comprises two main options:

(i) in-court insolvency proceedings, such as civil rehabilitation and corporate reorganization, which are court-led and permit majority-vote debt restructuring but often result in reputational and commercial harm due to their public nature; and

(ii) out-of-court workouts, which are, in principle, confidential and more flexible but require unanimous creditor consent, limiting their effectiveness.

Over the past two decades, Japan has introduced several structured out-of-court workout schemes, such as the Turnaround ADR (Alternative Dispute Resolution) procedure under the Act on Strengthening Industrial Competitiveness. These frameworks are characterized by their limited scope of participating creditors, primarily financial institutions such as banks, and the involvement of neutral experts who oversee both the overall process and the proposed debt adjustments. This impartial oversight enhances procedural objectivity. While limited creditor participation and confidentiality help preserve enterprise value, the requirement for unanimous consent remains an obstacle.

Recognizing the challenge and inspired by other countries’ laws, such as the UK’s Scheme of Arrangement and Restructuring Plan and Germany’s StaRUG, which allow for majority-approved debt restructuring subject to court confirmation before insolvency, Japan identified a gap in its legal framework.

To address this, METI developed a new pre-insolvency procedure through deliberations led by a subcommittee established under the Committee on New Direction of Economic and Industrial Policies, Industrial Structure Council. This new framework allows enterprises at risk of falling into financial distress but not yet insolvent to restructure only their financial debts, under the oversight of a neutral third-party organization and the court, thereby ensuring transparency, fairness, and minimal business disruption.

These efforts have culminated in the enactment of the Early Business Recovery Act, which lays the legal foundation for early-stage business turnarounds in Japan.

Ⅲ. Key Features of the New Framework

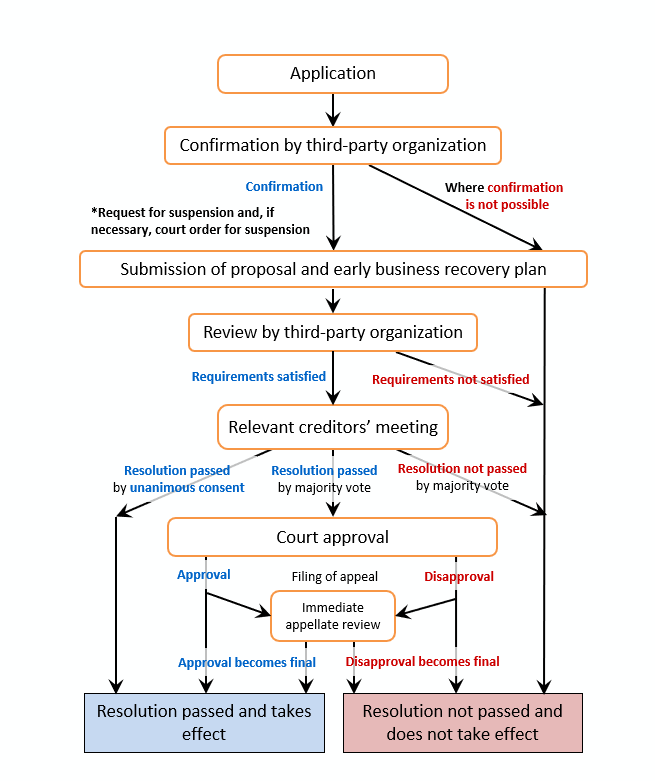

The main steps of the procedure are illustrated in the diagram below. The following sections provide an overview of each step.

1. Eligible Enterprises

The Act applies to “enterprises at risk of falling into financial distress,” which is the stage preceding the “economically distressed” status required under in-court insolvency procedures. This scope reflects the Act’s objective of promoting early and timely business recovery before insolvency occurs.

The eligibility criteria do not impose any limitations based on industry sector or enterprise size. However, the Act is primarily designed for cases where obtaining unanimous creditor consent, a prerequisite in current out-of-court workouts, proves challenging. Therefore, it is envisioned that the framework will be mainly utilized by large and mid-sized companies, particularly those with a relatively large number of financial creditors.

2. Eligible Claims

The claims eligible for modification under the Act are limited to financial debts held at the time of commencement by certain types of creditors, including financial institutions, insurance companies, licensed money lenders, government-affiliated entities, local governments, and licensed debt collection companies (servicers) that have acquired claims held by these entities.

Only the unsecured portions of secured claims are subject to modification by majority vote, preserving the legal priority of secured interests. However, the secured portions may still be subject to procedural measures such as temporary stays, even if they are excluded from the scope of modification.

3. Procedure Initiation – Confirmation by a Neutral Third-Party Organization

Under the Act, commencing the procedure requires confirmation by a neutral third-party organization designated by METI. Based on documentation submitted by the debtor, the organization must confirm that:

(i) the enterprise is at risk of falling into financial distress;

(ii) the claims proposed to be modified are loan or financial claims specified under METI ordinances that are held by eligible financial creditors, arising from causes prior to the confirmation;

(iii) it is not clearly unlikely that the required resolution will be approved at the creditors’ meeting;

(iv) the proposal is likely to be in the general interest of the affected creditors (i.e., satisfies the liquidation value test); and

(v) the debtor is not already subject to formal insolvency proceedings, such as bankruptcy or civil rehabilitation procedures.

Once these conditions are confirmed, the third-party organization must notify the affected creditors accordingly. If the debtor subsequently ceases to satisfy any of the prescribed requirements, the organization is required to revoke the confirmation, thereby terminating the procedure.

4. Temporary Stay Measures

4.1 Request for Temporary Stay by the Third-Party Organization

Following confirmation of eligibility under the Act, steps such as convening a creditors’ meeting will proceed. However, because enforcement or preservation of claims by affected creditors during this period could undermine equal treatment among creditors and disrupt a fair and orderly process, this risk is mitigated by a mechanism whereby, once confirmation has been granted, the third-party organization is authorized to request that all affected creditors temporarily refrain from enforcing their claims against the debtor until the procedure is concluded.

4.2 Court-Ordered Temporary Stay – Suspension of Enforcement and Realization of Security Interests

Because the third-party organization’s request outlined in section 4.1 is voluntary, it may not be sufficient to prevent creditors from pursuing enforcement actions or realizing security interests. Given that the Act introduces a majority-vote mechanism to modify claims, it is crucial to provide legal tools to suspend such actions.

Accordingly, where voluntary compliance is inadequate, the court may, under certain conditions, issue a binding stay order temporarily suspending individual enforcement actions or the realization of security interests.

As outlined in section 2, the secured portion of a claim is excluded from modification under the majority-vote framework. Nevertheless, in the absence of a stay on enforcement, secured creditors could enforce against essential business assets, undermining the debtor’s ability to continue operations or achieve a successful recovery, ultimately harming the interests of creditors as a whole. To prevent this, and give the debtor an opportunity to preserve and continue using the relevant assets through settlement or other arrangements with secured creditors, the court may order a suspension of the enforcement of security interests. This ensures a temporary pause in enforcement and creates space for negotiating repayment methods or other terms for the secured portion of the claims.

5. Submission of the Proposal and Early Business Recovery Plan

Within six months of receiving confirmation from the third-party organization, the debtor must prepare and submit:

(i) a written proposal detailing the terms of the proposed modification of creditor rights; and

(ii) an early business recovery plan.

The proposal must include provisions that modify all or part of the affected creditors’ rights. These provisions must also specify general criteria for the modification of affected claims, excluding the secured portion protected by security interests. Moreover, the proposed modifications must, in principle, treat all affected creditors equally.

The early business recovery plan must include the following information, as well as any additional items specified by ministerial ordinance:

(1) the circumstances that led to the need for a creditors’ resolution under this procedure;

(2) the business history and current operations of the debtor;

(3) the status and development of the debtor’s assets and liabilities;

(4) whether the affected claims are secured and, if so, a description of the security interests and the property subject to those interests;

(5) projections of the debtor’s assets, liabilities, revenues and expenditures; and

(6) matters relating to the debtor’s future business operations.

6. Review by the Third-Party Organization

The third-party organization must review the submitted proposal and the early business recovery plan to determine whether they satisfy the legal requirements, including the feasibility of debt repayment and consistency with the general interests of affected creditors (i.e., compliance with the liquidation value test). The organization must report the results of this review to the debtor. If it determines that the proposal, the plan, or the valuation of assets and liabilities does not meet the statutory requirements or if the debtor fails to cooperate without reasonable cause, the organization must revoke the initial confirmation, thereby terminating the procedure.

7. Resolution at a Creditors’ Meeting

7.1 Overview of the Meeting

Upon receiving the results of the review under section 6, the debtor must promptly convene a meeting of affected creditors to vote on the proposed modification.

In connection with the vote, the debtor must provide each affected creditor with a copy of the written proposal and, for reference purposes, with relevant materials such as the early business recovery plan and the results of the third-party review.

Furthermore, the debtor and the third-party organization are required to make efforts to provide affected creditors with any additional information necessary for making an informed decision on whether to approve the proposal. At the creditors’ meeting, the debtor must also ensure that affected creditors are given the opportunity to express their views.

Under the Act, each affected creditor is granted voting rights at the creditors’ meeting in proportion to the amount of their eligible claims. However, for secured claims, no voting rights are allocated for the claim portion that is covered by the value of the collateral and only the unsecured portion is counted toward voting rights.

7.2 Voting Threshold for Approval

If all voting creditors unanimously approve the proposal at the creditors’ meeting, the modification of claims becomes immediately effective without the need for court confirmation.

If unanimous consent is not obtained, the proposal may still be approved by a supermajority vote – specifically, by creditors representing at least 75% of the total voting rights. To protect small creditors, if a single creditor holds 75% or more of the total voting rights, approval also requires a majority of the number of creditors present at the meeting (i.e., a headcount test) in addition to the 75% threshold.

8. Court Approval of the Creditors’ Resolution

Where a resolution to modify creditor rights has been adopted by a supermajority vote, the debtor must, without delay, file a petition with the court seeking approval of the resolution, unless unanimous consent of all voting creditors has been obtained. Along with the petition, the debtor must submit the early business recovery plan and the third-party organization’s review report.

Given that the third-party organization has already reviewed the proposal prior to the vote, the court will assess whether the process was fair and properly conducted, whether the debtor is capable of performing its obligations under the modified claims, and whether the liquidation value test and other statutory requirements have been satisfied. The court will issue an approval order unless any of the following grounds for denial are present:

(i) the procedure or resolution violates applicable law, and the violations cannot be remedied, except where any procedural violations are minor;

(ii) the debtor is clearly unable to perform the obligations arising from the modified rights of affected creditors;

(iii) the resolution is adopted by unlawful means; or

(iv) the resolution is contrary to the general interests of the affected creditors (i.e., the liquidation value test).

The debtor and affected creditors may file an immediate appeal against the court’s decision to approve or deny the resolution.

Ⅳ. Conclusion

Japan’s newly enacted early business recovery framework represents a significant step in modernizing its approach to supporting businesses at risk of falling into financial distress, aligning with international practices while responding to domestic needs. Building on the practical experience of structured out-of-court workouts, the framework introduces a hybrid procedure that combines oversight by a neutral third-party organization with turnaround expertise and court involvement. By enabling majority-approved adjustments to financial debt, it aims to preserve enterprise value while ensuring procedural fairness through judicial oversight. With creditor protections and enhanced transparency, the new system offers a credible and practical tool for early business recovery, positioning Japan as a jurisdiction increasingly capable of facilitating timely and effective business turnarounds in a rapidly changing economic landscape.

- At the time of publication, the author is on secondment to the Corporate System Division, Economic and Industrial Policy Bureau, METI. The views expressed in this article are those of the author alone and do not necessarily reflect the official position of any organizations with which the author is affiliated.